You packed your bags, handed in your notice, and bought a one-way ticket — but your US real estate income doesn’t have to stay behind. Whether you already own rental property or you’re just starting to invest US real estate abroad expat passive income style, the good news is blunt: geography no longer controls your portfolio. From a condo in Chiang Mai to a co-working space in Lisbon, Americans living abroad are pulling thousands of dollars a month in passive income from US real estate — without setting foot in the country. This guide breaks down every layer of that stack: remote rentals, REITs, crowdfunding platforms, and the specific taxes you absolutely need to understand before you do any of it.

Why US Real Estate Is Still the Best Passive Income for Expats

:max_bytes(150000):strip_icc()/passive-real-estate-investing-8414890-final-28dd781515d345169a3b22754cfe3239.png)

Most Americans who move abroad obsess over their local cost of living — and rightly so. But the real wealth-building engine is still the US market. Here’s why that matters for expats specifically:

Dollar-denominated income in a world of volatile currencies. If you’re living in Mexico, Thailand, or Portugal, your rent in pesos, baht, or euros fluctuates with exchange rates. Your US real estate income in dollars doesn’t. When the local currency weakens — and they all do eventually — your dollar income buys more of everything.

The US real estate market has the deepest liquidity on earth. You can enter a position for $10 (via Fundrise), $100 (via Arrived Homes), or $5,000 (via RealtyMogul), or you can hold a physical rental property managed by a professional team while you’re eating tapas in Seville. No other country offers that range.

Leverage favorable tax geography. If you qualify for the Foreign Earned Income Exclusion (FEIE), you can exclude up to $126,500 (2024 limit, indexed annually) of foreign-earned income. That frees up more of your US passive income to compound — though passive rental income and REIT dividends are not covered by the FEIE and get taxed separately. More on that in the tax section.

The bottom line: for expats building a durable, location-independent income stream, US real estate remains the most battle-tested asset class available. The question isn’t whether to invest — it’s how to structure it so you’re not buried in paperwork or blindsided by a tax bill.

Option 1 — Keep Your Rental Property With a Property Manager (The Math)

Owning a physical rental property in the US while living abroad is entirely doable — millions of Americans do it. The key is offloading the operations entirely to a licensed property manager. Yes, there’s a cost. But the tradeoff is that you never need to be on-call at 2 AM when a pipe bursts.

What property managers typically charge:

| Service | Typical Cost |

|---|---|

| Monthly management fee | 8–12% of collected rent |

| Tenant placement fee | 50–100% of one month’s rent |

| Lease renewal fee | $150–$300 flat or ~25% of one month’s rent |

| Maintenance coordination markup | 10–15% on vendor invoices |

| Eviction coordination | $300–$500 flat (if needed) |

The math on a real rental: Say you own a single-family home in the Southeast US that rents for $2,000/month. Your mortgage (if any) is $950/month. After a 10% management fee ($200), taxes, insurance, and a modest maintenance reserve of $150/month, you’re netting roughly $550–$700/month in passive cash flow. That’s $6,600–$8,400/year — from one property — while you’re living on $1,500/month in Southeast Asia.

What to look for in a property manager abroad: Choose a National Association of Residential Property Managers (NARPM) member with experience managing properties for non-resident owners. Require monthly electronic statements, direct ACH deposits to your US bank account, and a maintenance spending limit (typically $200–$500) above which they must get your approval. Modern property management software like AppFolio and Buildium gives you real-time visibility from anywhere in the world.

Tax note: Rental income from US property is reported on Schedule E of your US federal return, regardless of where you live. You still deduct mortgage interest, depreciation, property taxes, insurance, and the full management fee. Depreciation alone on a $250,000 property reduces your taxable rental income by roughly $9,090 per year — even if the property is actually appreciating in value.

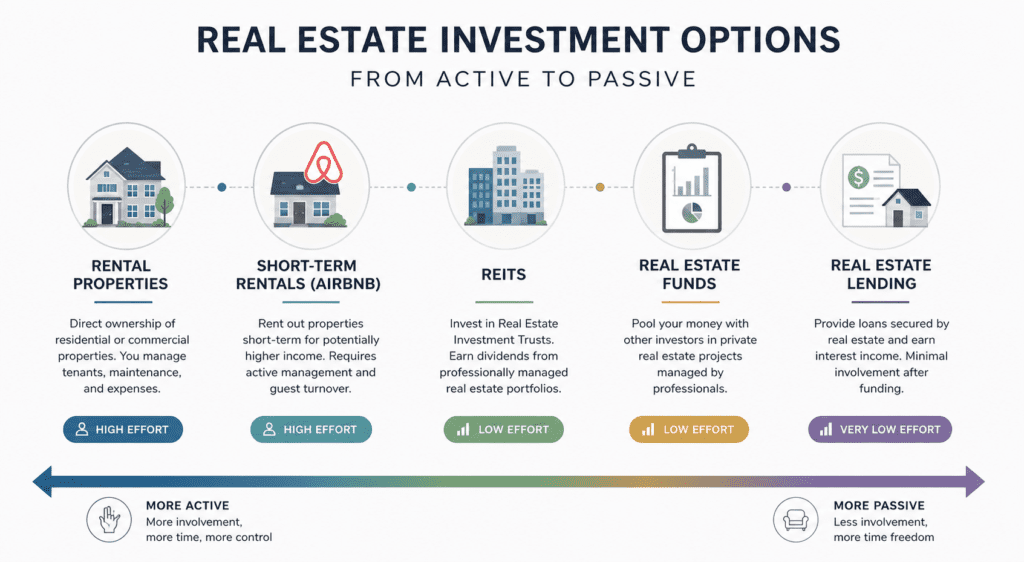

Option 2 — REITs: Wall Street Real Estate From a Beach in Thailand

Real Estate Investment Trusts (REITs) are the closest thing to set-it-and-forget-it real estate investing in existence. Buy shares through any US brokerage account (Fidelity, Schwab, Interactive Brokers — all accessible to expats), collect quarterly dividends, and never deal with a tenant. REITs for expats are especially compelling because there’s no minimum hold, no lock-up period, and you can liquidate within seconds during market hours.

Here’s how the major REIT ETFs stack up heading into late 2026:

| Ticker | Name | Dividend Yield (2026) | Expense Ratio | AUM | Minimum | Liquidity |

|---|---|---|---|---|---|---|

| VNQ | Vanguard Real Estate ETF | ~3.9% | 0.13% | $69.9B | None | Daily (exchange-traded) |

| SCHH | Schwab U.S. REIT ETF | ~2.8–3.6% | 0.07% | $9.7B | None | Daily (exchange-traded) |

| XLRE | SPDR Real Estate Select Sector ETF | ~3.3–3.5% | 0.08% | $7.1B | None | Daily (exchange-traded) |

| REM | iShares Mortgage Real Estate ETF | ~9.7% | 0.48% | Smaller | None | Daily (exchange-traded) |

| O (Realty Income) | Individual REIT — Monthly Dividends | ~5.5% | N/A | $50B+ mkt cap | ~$50/share | Daily (NYSE) |

For most expats, VNQ is the workhorse pick. With ~$70 billion in assets, 155 holdings, and a 3.9% trailing yield at a 0.13% expense ratio, it gives you broad exposure to apartment REITs, industrial REITs, data centers, retail, and healthcare real estate in a single trade. If you want to squeeze costs further, SCHH’s 0.07% expense ratio is the cheapest pure-REIT ETF on the market.

For income chasers: Realty Income (ticker: O) is the gold standard individual REIT for yield-focused investors. It pays monthly dividends and has raised them 127+ consecutive times. At a ~5.5% yield on a $50,000 position, that’s ~$229/month deposited directly into your account — no tenants, no maintenance calls, no FIRPTA complications on sale if you hold through a brokerage.

Tax note for expats on REITs: REIT dividends are generally classified as ordinary income (not qualified dividends), meaning they’re taxed at your marginal rate. They are also subject to the 3.8% Net Investment Income Tax (NIIT) if your modified adjusted gross income (MAGI) exceeds $200,000 (single) or $250,000 (married filing jointly). The FEIE does not reduce your MAGI for NIIT purposes — a frequently misunderstood point that surprises many expats at tax time.

Option 3 — Real Estate Crowdfunding Platforms (Fundrise, Arrived, RealtyMogul)

Real estate crowdfunding platforms sit between physical ownership and REITs — you get exposure to actual properties (not just a real estate index), without the operational headaches of being a landlord. Here’s an honest breakdown of the three most relevant platforms for expats in 2026:

| Platform | Minimum | Annual Fees | Target / Historical Returns | Liquidity | Focus |

|---|---|---|---|---|---|

| Fundrise | $10 | 1% annual (advisory + management) | ~7% long-run avg; +1.5% in 2022, -7.45% in 2023, recovering 2024–2025 | Low — 5+ year recommended hold; early redemption 1% penalty within first 5 years | eREITs, eFunds, residential & commercial |

| Arrived Homes | $100 | ~3.5% sourcing + 1% AUM annual | Q1 2026 dividend yield ~3.6%; ~18.6% total return on 173 exited properties (over hold period) | Low — 5–7 year hold; quarterly sellback program, not guaranteed | Single-family rentals & vacation rentals |

| RealtyMogul | $5,000 (REITs); $25,000+ (private placements) | Multi-tier (1–1.5% AUM + property-level fees) | Income REIT targets 6–8% annual distributions; private placements target higher IRR | Medium — quarterly redemption after 3-year hold at full NAV | Commercial real estate, multifamily, retail |

Fundrise: The entry point for anyone who wants to invest US real estate abroad expat passive income style with as little as $10. The platform’s “Flagship Fund” focuses on residential real estate and has historically targeted 7–10% annual returns. The catch: you’re investing in a non-traded REIT, which means liquidity is limited. Treat Fundrise as a 5-year+ commitment. Distributions are paid quarterly and hit your linked bank account automatically.

Arrived Homes: The most transparent option for single-family rental exposure. You can browse individual properties, see the specific address, projected rent, and historical returns before committing $100. Q1 2026 dividend yields averaged about 3.6% annually, which lags high-yield savings accounts — but you also get property appreciation. The 173 exited properties as of early 2026 showed an 18.6% total return over the hold period, though that’s not an annualized figure.

RealtyMogul: Best for accredited investors who want commercial real estate exposure with more institutional-grade deal flow. The Income REIT has targeted 6–8% annual distributions and made monthly payouts — meaningful for expats building a monthly income stack. The $5,000 minimum and multi-tier fee structure make it less beginner-friendly, but the deal quality and transparency are above average for the crowdfunding space.

One important note for expats: All three platforms require a US Social Security Number (SSN) or ITIN and a US bank account. If you’ve maintained a US bank account (Schwab, Charles Schwab Bank, and Wise work well for expats), you’re set. If you’ve closed everything, you’ll need to re-establish US banking infrastructure before investing.

The Tax Reality: What You Owe on US Real Estate Income While Abroad

This is the section most expat real estate content skips over or gets wrong. Here’s the full, honest picture:

Schedule E and rental income: US rental income is always reported on Schedule E of your Form 1040, regardless of where you live. You deduct mortgage interest, property taxes, insurance, depreciation, management fees, and repairs. Net rental income flows to your regular income. Net losses may be limited by passive activity loss rules — generally, you can deduct up to $25,000 in rental losses against ordinary income if your MAGI is under $100,000, phasing out completely at $150,000.

FIRPTA withholding: The Foreign Investment in Real Property Tax Act (FIRPTA) requires buyers to withhold 15% of the gross sales price when a non-US resident sells US real estate. This doesn’t mean you pay 15% tax — it’s a withholding mechanism, and you claim it back when you file your return. But it’s a cash-flow shock many expats don’t anticipate. If your actual capital gains tax is lower than the FIRPTA amount withheld, you get a refund. File Form 8288-B before closing to request a reduced withholding certificate if your gain is smaller than 15% of the sale price.

Net Investment Income Tax (NIIT): If your MAGI exceeds $200,000 (single) or $250,000 (married filing jointly), a 3.8% NIIT applies to net rental income, REIT dividends, and capital gains from real estate sales. This is on top of regular income tax. One large gain or a high rental income year can easily push you over the threshold. Plan for it.

FEIE and passive income: The Foreign Earned Income Exclusion (FEIE) — up to $126,500 for tax year 2024 — covers only earned income (wages, self-employment). Rental income, REIT dividends, and crowdfunding distributions are passive investment income and are specifically excluded from the FEIE. You owe US tax on them regardless of the FEIE election.

1031 exchange for expats: A 1031 exchange lets you defer capital gains taxes by rolling proceeds from one investment property into another “like-kind” property within strict timelines (45 days to identify, 180 days to close). Expats can use 1031 exchanges — your residency status doesn’t disqualify you. What matters is that the properties are US-based and the exchange is properly structured through a qualified intermediary. This is one of the most powerful tax-deferral tools available to expat real estate investors.

State taxes: Some states — particularly California, New York, and New Jersey — tax non-residents on rental income sourced from property within the state. If you own a rental in California and moved abroad, California still wants its cut. States with no income tax (Texas, Florida, Nevada) obviously don’t have this issue.

How to Invest US Real Estate Abroad Expat Passive Income Style — The $3,000/Month Stack

Here’s a concrete model for how an expat could stack $3,000/month in passive real estate income using all three layers. This is not a guaranteed outcome — it’s a framework based on current market yields and platform data as of 2026.

| Income Layer | Vehicle | Capital Required | Est. Monthly Income |

|---|---|---|---|

| Layer 1 — Rental property | 1 single-family home, property managed | $150,000–$300,000 (down payment on leveraged purchase) | $550–$900 |

| Layer 2 — REIT dividends | VNQ + Realty Income (O) | $200,000 invested ($100K each) | ~$750–$925/month ($9,000–$11,100/year at 4.5–5.5% blended) |

| Layer 3 — Crowdfunding | Fundrise Flagship + RealtyMogul Income REIT | $50,000 ($25K each) | ~$250–$350/month at 6–8% target distributions |

| Layer 4 — Individual REITs | Realty Income (O) + STAG Industrial | $50,000 | ~$220–$280/month at 5–5.5% yield |

Total estimated monthly income: $1,770–$2,455 on a ~$500,000 total capital base. To hit $3,000/month consistently, you’d need either a second rental property, a larger REIT position (roughly $350,000–$400,000 at 4% yield), or a combination of higher-yield instruments like mortgage REITs (REM at ~9.7% — higher risk) or Realty Income at scale.

The key insight: none of these income streams require you to be physically present in the United States. The rental property runs on your property manager’s schedule. REIT dividends hit your brokerage account quarterly or monthly. Crowdfunding distributions are wired directly to your US bank account. The entire stack is designed for passive rental income abroad — you show up once a year at tax time (or hire a US expat CPA to handle that too).

Building it over time: If you’re starting from scratch rather than cashing out an existing portfolio, start with Fundrise ($10) and Arrived ($100) to learn the platforms while building capital. Layer in VNQ in a Schwab or Fidelity account with whatever you have. Add physical property when you have enough for a down payment and have identified a strong property management company in your target market. This is a 3–5 year build, not a weekend project — but every dollar you compound now is a dollar that works while you sleep.

The Expat Real Estate Stack — Start Today, Not After You Land

The single biggest mistake expats make with US real estate is waiting — either waiting until they’ve “settled in” abroad, or selling everything before they leave because it feels complicated. Don’t do either. The complication is front-loaded: set up the property manager, open the brokerage account, understand the tax structure. Once that infrastructure is in place, the income runs on autopilot.

Here’s your action list before you move — or right now if you’re already abroad:

1. Keep your US bank account open. Schwab Bank reimburses ATM fees worldwide and has no foreign transaction fees. It’s the gold standard for expat banking. You need it for all US investment platforms.

2. Open a brokerage account before you leave. Fidelity, Schwab, and Interactive Brokers all allow non-resident Americans to hold accounts. Some brokerages will close accounts once they discover your foreign address — open before you go.

3. Start with VNQ or SCHH in your brokerage. Even $5,000 in VNQ at 3.9% pays roughly $195/year — that’s a night in a nice hotel in Southeast Asia, funded by your portfolio. Start small, build the habit.

4. Open a Fundrise account with $10. Yes, $10. Get familiar with the platform, the dashboards, the quarterly distributions, and how the tax documents are issued. Scale up once you trust the system.

5. Hire a US expat CPA. Firms like Greenback Tax Services or Bright!Tax specialize in Americans abroad. The cost ($300–$800/year for a typical expat return) pays for itself the first time you avoid a FIRPTA surprise or correctly apply depreciation to reduce your Schedule E income.

6. If you already own property, interview property managers now. Find a NARPM-certified manager in your market, set up the ACH wire, and confirm the reporting cadence before you board the plane.

The dream of living abroad while your US real estate pays for your life is not a fantasy. It’s a financial architecture problem — and it’s one of the more solvable ones. The Americans who pull it off aren’t smarter than you. They just started earlier.

Sources: Lofty.ai — Arrived vs Fundrise vs RealtyMogul 2026 Comparison | Bambridge Accountants — Net Investment Income Tax for Expats | Dividend Growth Lab — Best REIT ETFs 2026 | WTOP News — Best REIT ETFs for 2026 | Motley Fool — VNQ vs SCHH June 2026. All returns and yields represent past performance and are not guarantees of future results. This article is for informational purposes only and does not constitute financial or tax advice. Consult a qualified tax professional before making investment decisions.