If you live in California, New York, or Illinois, you already know the feeling: you earn a solid income, you work hard, and somehow you still feel financially squeezed. There is a mathematical reason for that. A California resident earning $150,000 faces a combined marginal rate — federal, state, and FICA — of roughly 47 cents on every additional dollar earned. In New York City, a $200,000 earner can hand over more than $74,000 in combined federal, state, and city taxes in a single year. In Illinois, a homeowner in Cook County can pay an effective property tax rate that exceeds 3%. These are not edge cases. They are the baseline reality for millions of residents in the three highest-cost, highest-tax states in the country. The California New York Illinois moving abroad financial savings 2026 conversation is not about running away from something. It is about recognizing what the numbers actually say.

This post is not financial advice. It is an honest look at the math — income taxes, property taxes, cost of living — that explains why residents of these three states are leaving at a faster rate than almost anywhere else in the nation, and why moving abroad amplifies that financial relief in ways that domestic relocation simply cannot match.

California: 47 Cents on Every Additional Dollar

California has the highest state income tax rate in the United States: 13.3% at the top, but the bracket that hits most upper-middle-class earners starts earlier than people expect. The 9.3% rate kicks in at $66,295. At $338,639 you are already at 10.3%. Stack the federal 24% bracket, add FICA at roughly 7.65%, and a California resident earning $150,000 is looking at a combined marginal rate somewhere around 47.3% on each additional dollar. Nearly half of every raise, every side hustle payment, every freelance invoice disappears before it touches your bank account.

Then there is housing. The statewide median home price sits at approximately $800,000. In San Francisco it is closer to $1.2 million. In Los Angeles, $900,000. California’s Proposition 13 protects long-term owners from dramatic reassessments, but if you are buying today, you are paying roughly 1% of the purchase price in annual property taxes — $8,000 per year on an $800,000 home. That is before homeowners insurance, HOA fees, or the reality that California’s insurance market has become increasingly unaffordable as major carriers exit the state.

None of this is speculative. California has experienced a net outmigration of approximately 1.7 million residents since 2020 — the largest domestic population loss of any state. People are not leaving because they dislike the weather. They are leaving because the math no longer works.

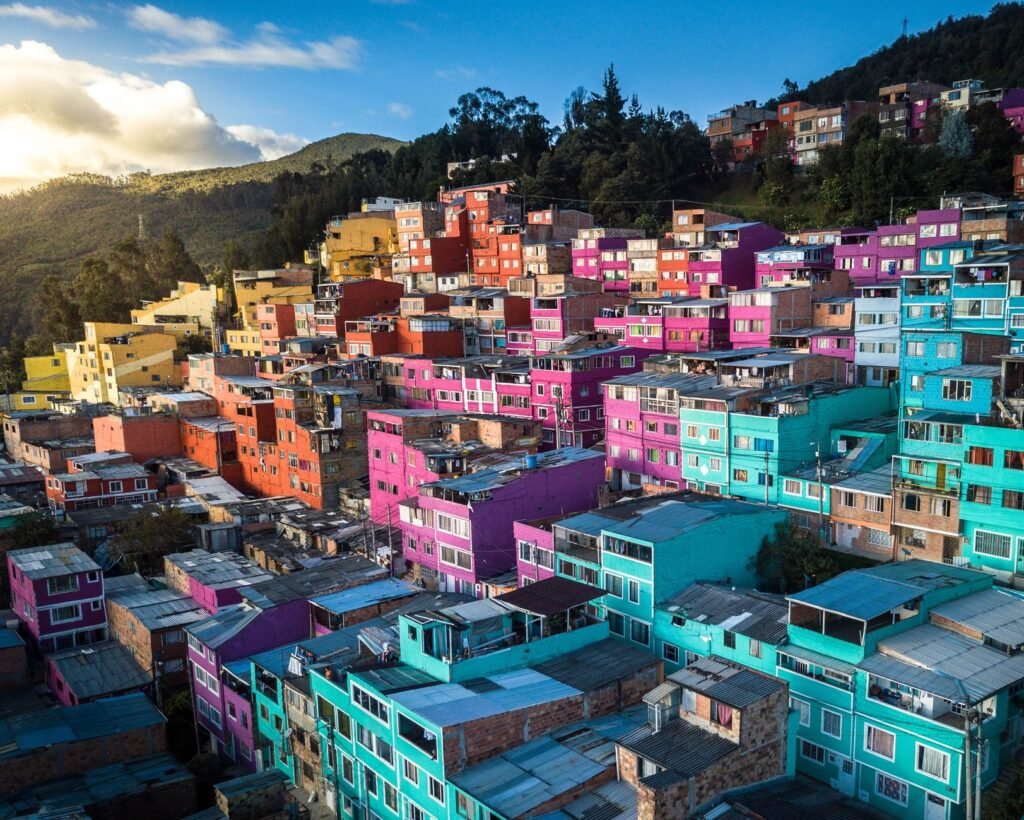

Now consider what changes if a California-based remote worker or self-employed professional establishes legal residency in Medellín, Colombia. Colombia operates on a territorial tax system — foreign-sourced income is not taxed domestically for most foreign residents. That same $150,000 earner eliminates the 9.3% California state tax: $13,950 per year, immediately. If they are self-employed and establish residency in a country covered by a US totalization agreement, the FICA picture changes as well. On the cost-of-living side, a comfortable one-bedroom apartment in El Poblado or Laureles runs $800 to $1,200 per month. Compared to $3,000+ in San Francisco or $2,500+ in Los Angeles, the annual rent savings alone can run $18,000 to $36,000. Total annual savings for a California resident making this move: conservatively $33,000 and realistically as high as $61,000 per year.

One important caveat: California’s Franchise Tax Board is among the most aggressive state tax authorities in the country when it comes to auditing departing residents. Domicile severance — cutting California ties cleanly — requires deliberate steps, which we cover in detail in our separate guide on the California exit process.

New York: When the City Takes Its Cut on Top of the State’s Cut

New York City residents face something that most Americans in other states do not: a three-layer tax structure. Federal income tax runs up to 37%. New York State adds up to 10.9%. Then the city itself adds its own income tax at 3.876%. For a high earner, the combined marginal rate exceeds 50%. That is not a talking point — it is arithmetic.

A New York City resident earning $200,000 per year pays approximately $74,000 in combined federal, state, and city income taxes. That leaves $126,000 before rent, food, transportation, and everything else. The median one-bedroom rent in Manhattan and the surrounding boroughs tracked at $3,814 per month in 2026. Annual rent alone: $45,768. After taxes and rent on a $200,000 income, you are working with roughly $80,000 for all other expenses in one of the most expensive cities on earth.

Portugal’s Non-Habitual Residency (NHR) regime — now in a revised form as of 2024 — offers qualifying foreign-sourced income a 20% flat rate, with various exemptions and structures that can reduce the effective burden significantly below what New York imposes. For a $200,000 earner whose income is primarily foreign-sourced, moving to Lisbon could generate $20,000 to $40,000 per year in combined state and city tax savings alone. Add the cost-of-living differential: a well-appointed one-bedroom apartment in Lisbon’s Príncipe Real or Alfama neighborhood runs $1,200 to $1,800 per month — less than half of what the same quality of life costs in Manhattan. The combined annual financial benefit for a New York City resident relocating to Lisbon: $32,000 to $60,000 per year.

New York State’s net migration has been negative every year since 2020. This is not a pandemic anomaly. The structural math has not improved, and for residents asking whether there is a better financial arrangement available to them somewhere else in the world, the answer is increasingly clear.

Illinois: The Property Tax Problem No One Wants to Talk About

Illinois does not get the same national attention as California or New York when people discuss high-tax states, but the numbers tell a story that Illinois residents know intimately. The state income tax is a flat 4.95% — not progressive, everyone pays it regardless of income level. By itself, that is not catastrophic. The crisis in Illinois is the property tax.

Illinois has the second-highest effective property tax rate in the United States at 2.08%. On a $400,000 home, that is $8,320 per year in property taxes alone. In parts of Cook County — which includes Chicago and its immediate suburbs — the effective rate in some townships exceeds 3%. A $400,000 property in those areas can carry a property tax bill above $12,000 annually. These are recurring, unavoidable costs that compound every year you own the property.

The underlying reason these property taxes keep climbing is no secret to long-term Illinois residents: the state is carrying approximately $237 billion in unfunded pension liabilities. That gap does not close on its own. It gets serviced through local property taxes, which means the structural pressure on Illinois property owners is not easing — it is increasing. Anyone who believes 2026 property taxes are the ceiling, rather than a waypoint, has not been following Springfield for long.

For Chicago renters, the picture is different but not more comfortable. A one-bedroom apartment in Lincoln Park, Wicker Park, or the West Loop runs $1,950 to $2,400 per month — $23,400 to $28,800 per year. The same monthly rent in Medellín: $800 to $1,200. The annual rent savings for a Chicago renter who moves to Medellín falls between $12,000 and $16,800 — and that is before accounting for lower food costs, transportation, and daily expenses. Illinois residents considering this move are often renters who feel the double squeeze of high rent and no path to affordable homeownership given what property taxes do to ownership costs.

California, New York & Illinois Moving Abroad: Financial Savings Summary

The table below consolidates the estimated annual savings for a representative earner from each state, comparing their current situation to a realistic international relocation. All figures are estimates based on publicly available tax rates and cost-of-living data. Individual circumstances vary.

| State | Destination | Est. State/City Tax Saved | Est. COL Saved | Est. Annual Total |

|---|---|---|---|---|

| California ($150K earner) | Medellín, Colombia | $13,950–$22,500 | $18,000–$36,000 | $33,000–$61,000 |

| New York City ($200K earner) | Lisbon, Portugal | $20,000–$40,000 | $12,000–$20,000 | $32,000–$60,000 |

| Illinois / Chicago (renter, $100K earner) | Medellín, Colombia | $4,950–$8,000 | $12,000–$16,800 | $16,950–$24,800 |

These are not lottery-ticket scenarios. They are the result of two compounding factors — lower tax jurisdictions abroad and dramatically lower costs of living — that align unusually well for residents of high-COL, high-tax US states. The residents of California, New York, and Illinois carry the highest combined financial burden in the country. They also have the most to gain from rearranging where they live.

The Tradeoffs Are Real — But So Is the Math

No honest case for moving abroad ignores what gets left behind. Family proximity is not a line item you can offset with savings. Career networks built over years in New York or San Francisco do not transfer automatically. Cultural familiarity — knowing how to navigate a healthcare system, understanding local legal norms, feeling at home in a neighborhood — takes real time to rebuild in a new country. These are legitimate costs, and they belong in any serious analysis.

But here is what is also true: $33,000 to $61,000 per year in recovered income is not a minor optimization. Over five years, that is $165,000 to $305,000 — capital that can fund a business, eliminate debt, build an investment portfolio, or simply reduce the baseline stress that comes with earning well and still feeling financially exposed. For many people in California, New York, and Illinois, the conversation is not about escaping something but about reclaiming a financial margin that the current arrangement has steadily eroded.

The residents who feel this most acutely are not struggling — they are the ones who earn enough to be hit hardest by marginal rates, own enough to feel property taxes as a recurring wound, and pay enough in rent to understand that housing cost alone is consuming what should be generational wealth-building capital. If that description fits, you are not misreading your situation. The math is telling you something real.

What Comes Next

The financial case laid out here — anchored in California New York Illinois moving abroad financial savings 2026 — is the starting point, not the complete picture. Understanding the savings is step one. Executing the move cleanly involves visa selection, tax residency establishment, banking restructuring, and for California residents specifically, a deliberate process of severing FTB ties. Each of those steps has its own playbook, and the details matter.

FundYourExit covers each stage of this process in dedicated guides. If you are a California resident navigating the Franchise Tax Board’s departure audit risk, a New York City earner evaluating the NHR regime in Portugal, or an Illinois homeowner calculating whether selling and relocating abroad pencils out after property taxes and pension-driven future increases, the resources are here. The numbers above are not a fantasy. They are the arithmetic of a decision that tens of thousands of Americans from these three states are actively making right now.