Five years from now you could return to the United States with your mortgage balance cut in half — or gone entirely. That result comes from a deliberate geoarbitrage mortgage payoff strategy moving abroad savings into your loan every month: live in a low-cost city overseas, live well on a fraction of your current spending, and redirect the difference straight to your mortgage principal. The math is unambiguous, and the plan is more achievable than most people imagine.

This post walks through the exact numbers on a $280,000 mortgage, a concrete five-year scenario based in Medellín, Colombia, and what to do with the savings you don’t put toward the loan. By the end you will have a framework you can adapt to your own situation — whether you’re a remote worker, freelancer, small business owner, or early retiree with US-source income.

Disclaimer: This post is for informational purposes only and does not constitute financial, tax, or legal advice. Consult qualified professionals before making financial decisions.

The Mortgage Math No One Talks About

Most homeowners know their monthly payment but have never looked at their total interest bill. On a $300,000 mortgage at 6.5%, the standard 30-year payment is roughly $1,896 per month in principal and interest. Over the life of the loan you will hand the bank approximately $382,560 in interest alone — more than the original loan. You borrow $300,000 and ultimately pay back $682,000.

The good news: extra principal payments are one of the most powerful financial levers available to a homeowner. Every dollar you send above the required payment reduces principal immediately, cuts years off the loan term, and saves you the interest that would have compounded on that dollar for decades. The table below shows exactly what happens when you add $500, $1,000, $1,500, or $2,000 per month to a $300,000 loan at 6.5%.

| Extra Payment/Month | Payoff Timeline | Total Interest Paid | Interest Saved vs. 30-Year |

|---|---|---|---|

| $0 (baseline) | 30 years | ~$382,560 | — |

| +$500/month | ~19 years | ~$247,000 | ~$135,000 |

| +$1,000/month | ~13 years | ~$173,000 | ~$210,000 |

| +$1,500/month | ~8 years | ~$92,000 | ~$290,000 |

| +$2,000/month | ~7 years | ~$72,000 | ~$310,000 |

Adding $1,500 per month slashes the loan from 30 years to roughly 8, saving about $290,000 in interest. Adding $2,000 per month takes it down to 7 years and saves $310,000. These are not rounding errors — they are life-changing numbers. The question is simply: where do you find an extra $1,500 to $2,000 per month? For most Americans living in a major city, the answer is geoarbitrage.

What Geoarbitrage Actually Does to Your Budget

Geoarbitrage is the practice of earning income in a strong currency — typically US dollars — while living in a country where costs are a fraction of what they are at home. The gap between what you earn and what you spend is the engine that makes the accelerated payoff possible.

A comfortable life in Austin, Texas runs $3,500 to $4,500 per month for a single person or couple when you add up rent, food, transportation, utilities, health insurance, and entertainment. The same comfortable lifestyle in Medellín, Colombia’s Laureles neighborhood costs $1,200 to $1,500 per month — sometimes less. That is a gap of $2,000 to $3,000 every single month. Redirected to your mortgage, that gap becomes your geoarbitrage savings redirect mortgage machine.

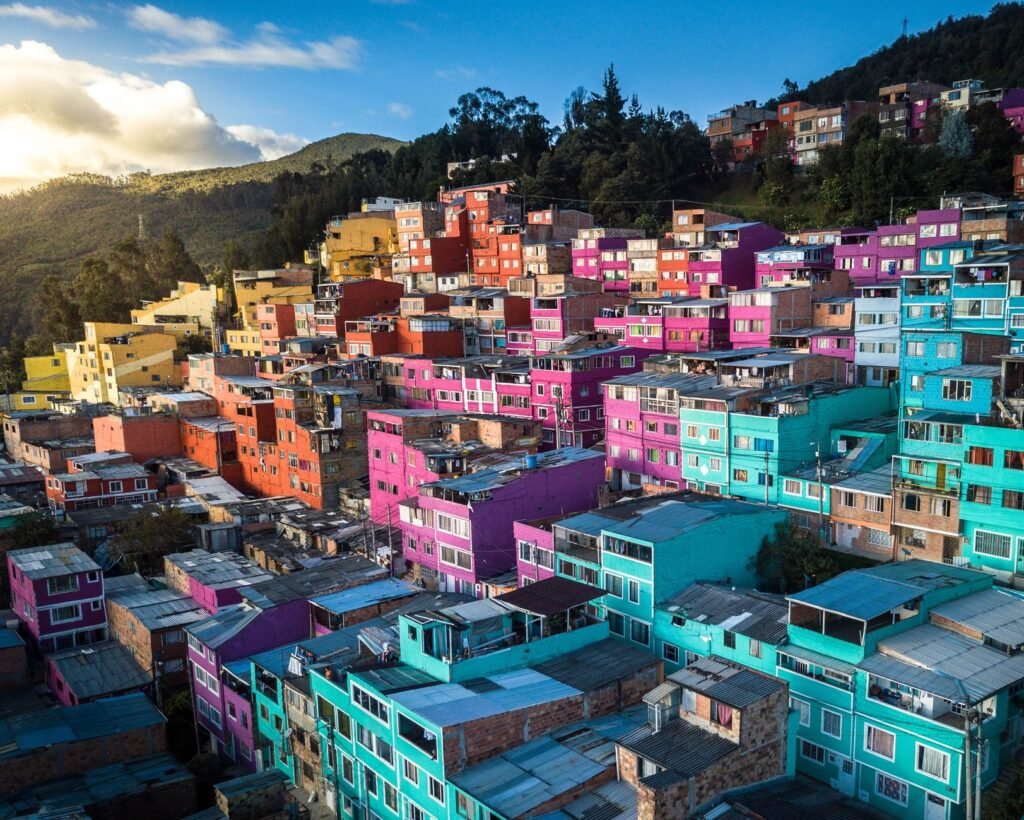

Medellín is a particularly strong choice for this strategy. The city sits at 5,000 feet elevation, giving it near-perfect spring-like weather year-round. It has a large, established expat community, reliable high-speed internet throughout Laureles and El Poblado, direct flights to Miami and multiple US hubs, and a cost of living that has remained favorable even as the city has grown in popularity. A furnished one-bedroom apartment in Laureles runs $500 to $700 per month. Groceries for two cost $200 to $300. Dining out at local restaurants is $4 to $8 per meal.

The 5-Year Medellín Scenario — A Concrete Case Study

Here is what the pay off mortgage faster moving abroad strategy looks like with real numbers attached to a real person.

Starting situation: You are a remote worker currently renting in Austin for $2,000 per month. You own a home worth $350,000 with $280,000 remaining on a 6.5% mortgage. Your monthly mortgage payment (principal and interest) is approximately $1,896. You have a US income of $5,500 to $6,500 per month.

The move: You relocate to the Laureles neighborhood of Medellín. Your total monthly spend — rent, food, transportation, health insurance, internet, entertainment — lands at $1,300. That frees up roughly $2,700 to $3,000 per month compared to your Austin lifestyle.

The allocation: You direct $1,500 of that freed-up cash straight to mortgage principal each month. The remaining $1,200 to $1,500 goes into a brokerage account or index fund.

| Year | Mortgage Balance | Extra Principal Paid | Investment Account |

|---|---|---|---|

| Start | $280,000 | — | $0 |

| Year 1 | ~$258,000 | $18,000 | ~$15,500 |

| Year 2 | ~$234,000 | $18,000 | ~$32,000 |

| Year 3 | ~$209,000 | $18,000 | ~$50,000 |

| Year 4 | ~$181,000 | $18,000 | ~$69,000 |

| Year 5 | ~$150,000 | $18,000 | ~$90,000+ |

After five years you return to the United States with a mortgage balance of approximately $150,000 — down from $280,000. You’ve eliminated $130,000 in principal (the $90,000 in extra payments plus normal amortization on an accelerated schedule), and you have $90,000 or more sitting in index funds. The home you left behind at $350,000 has likely appreciated to $400,000 to $420,000 at a conservative 3% annual rate. Your net worth has increased by roughly $200,000 or more in five years — not counting your continued US income.

This is the power of the accelerate mortgage payoff expat approach: you’re not giving up wealth to live cheaply. You’re building more of it, faster, precisely because you’re living cheaply.

What About Renting Your Austin Home While You’re Gone?

Many people executing this strategy don’t leave their home vacant — they rent it. In the Austin scenario, a $350,000 home in a desirable neighborhood could realistically fetch $2,400 per month in rent. Here’s how that pencils out:

| Item | Monthly |

|---|---|

| Rental income | +$2,400 |

| Mortgage P&I | −$1,896 |

| Property management (10%) | −$240 |

| Insurance & property tax (est.) | −$350 |

| Maintenance reserve (1% annual / 12) | −$292 |

| Net monthly cash flow | ~−$378 to breakeven |

The rental income essentially covers the mortgage and carrying costs. You’re not cash-flow positive from the rental, but you’re also not paying your US mortgage out of pocket. Meanwhile, you’re living on $1,300 per month in Medellín while your US income of $5,500 to $6,500 per month continues to flow in. That means $2,000 or more per month is available after Medellín living costs — every dollar of which can go toward extra principal payments or investments.

The rental path also preserves optionality. Your tenant is covering the loan’s normal amortization. You’re applying additional lump sums whenever you choose. And when you return, you can move back in, sell, or keep it as a long-term rental — with far less debt attached than when you left.

What To Do With the Rest of Your Savings

Not every dollar of your geoarbitrage surplus needs to go to the mortgage. If your mortgage rate is below the long-run expected return from a diversified index fund, the math slightly favors investing. Here’s the comparison:

| Use of $1,500/Month | 5-Year Outcome | Effective Return |

|---|---|---|

| Extra mortgage principal | ~$90,000 in debt eliminated | 6.5% guaranteed (after-tax equivalent) |

| Index fund at 7% avg return | ~$108,000 portfolio | 7% (before tax, variable) |

| Split: $1,000 mortgage + $500 investing | $60K debt reduction + $36K portfolio | Blended, diversified approach |

At a 6.5% mortgage rate, paying down the loan is roughly equivalent to a guaranteed, after-tax 6.5% return — genuinely competitive. If your rate were 3%, the calculus would shift sharply toward investing. At 6.5%, either path is defensible, and a blended approach — aggressively paying the mortgage while keeping some money in the market — gives you both debt reduction and liquidity.

The extra mortgage payments abroad strategy works best as a system: automate a fixed extra payment each month so it becomes invisible, then invest whatever remains. After five years abroad you will not miss the money, but you will absolutely notice that your mortgage balance looks nothing like what it would have been if you’d stayed in Austin.

Who This Strategy Works For

The geoarbitrage savings redirect mortgage approach requires a few things to be in place:

US-source income you can take abroad. Remote employees, freelancers, consultants, small business owners, and people with investment or rental income all qualify. If your income is location-dependent, the strategy requires solving that problem first — but many people have already done it.

A mortgage you want to eliminate. The strategy is most powerful when your mortgage rate is 5.5% or higher. Below that threshold, the investment alternative becomes increasingly attractive.

Willingness to live differently for a defined period. This is a five-year plan, not a permanent sentence. Medellín is genuinely a great city — lively, warm, with excellent food and a growing creative economy. But you need to be honest with yourself about whether you can sustain it for the timeframe required.

A clear return plan. The strategy works because it has a defined endpoint. At the end of year five you have options: come home to a nearly paid-off mortgage, extend abroad for another year or two to finish the job, sell the home and capture the equity potentially tax-free under IRS Section 121 (which allows up to $250,000 in capital gains exclusion for a primary residence, or $500,000 for married couples, if you’ve lived in it two of the last five years), or convert it permanently to a rental.

Running the Numbers on Your Own Situation

The framework generalizes beyond Medellín. Chiang Mai, Thailand runs $800 to $1,200 per month. Lisbon’s suburbs and the Algarve region of Portugal run $1,500 to $2,000. Tbilisi, Georgia is under $1,000. Oaxaca, Mexico is $900 to $1,400. Each of these cities offers reliable internet, established expat communities, and a cost structure that creates the same gap-against-US-income that Medellín does.

The math you need to run is straightforward: take your current monthly spend, subtract what you’d spend in your target city, and multiply by 60 months. That is your five-year geoarbitrage dividend. Then split it between mortgage prepayments and investments in whatever ratio lets you sleep at night. Run the prepayment amount through a mortgage amortization calculator to see what your balance looks like at month 60. The number will likely surprise you.

Most people who do this calculation realize they are one decision away from a fundamentally different financial trajectory. The decision is not complicated — it is just uncommon. That is what makes it powerful.

The Bottom Line

The 5-year Medellín plan is not about deprivation. It is about leverage — using the global income gap to accomplish in five years what would otherwise take twenty. A $280,000 mortgage at 6.5% is a $130,000 anchor on your future if you make minimum payments for decades. Applying a serious geoarbitrage mortgage payoff strategy — redirecting $1,500 per month in extra principal payments from a city where $1,300 covers everything you need — transforms that anchor into a manageable $150,000 balance, mostly equity, when you return.

The Medellín savings plan US mortgage strategy works because geography is the one variable in your financial life that you can change dramatically and quickly. Your income stays the same. Your mortgage rate stays the same. But your cost of living drops by 60 to 70 percent — and every dollar of that difference has somewhere productive to go.

Run your own numbers. Pick your city. Set a timeline. The mortgage does not care where you live while you pay it off.